Cyprus tax legislation in brief for individuals and non-domicile.

Taxation of individuals

Individuals resident in Cyprus are subject to tax on worldwide income. An individual is resident if he spends more than 183 days in Cyprus during the calendar year which is also the fiscal year.

Another option for the Cyprus tax residency is the so called “60 day rule”.

An individual is a tax resident of Cyprus under this rule if he fulfills the following requirements:

• Does not reside in any other state for longer than 183 days;

• Not considered tax resident by any other state;

• Resides in Cyprus at least 60 days;

• Has ties to Cyprus. This includes carrying out a business in Cyprus, being employed in Cyprus, or holding a director position in a Cyprus tax resident company.

• Maintains a permanent residential property in Cyprus, either owned or rented.

Cyprus offers attractive tax incentives to individuals who move to Cyprus. The persons who are born to non-Cypriot parents and come to live in Cyprus are non-domiciled tax residents (Non-Doms) during the first 17 years of their stay in Cyprus. The Non Domiciliary status is available to any one who is tax resident in Cyprus under either of the above two tax residency options.

A simple registration procedure needs to be complied for such individuals to avail themselves of the advantages offered in Cyprus to Non-Doms. Income in Cyprus is taxes either under the Income Tax (IT) law or the Special Defence Contribution (SDC) law or sometimes under both. The Non-Doms are not subject to SDC on dividend, interest, and rental income only. As a result, dividend will never be taxed. Interest if earned as part of an interest earning trading activity will be taxed under IT, but it will not be taxed at all when the interest income is of passive nature. Rental is taxed both under IT and SDC in the normal way, but it will not be taxed for SDC in the case of a Non-Dom.

Income tax

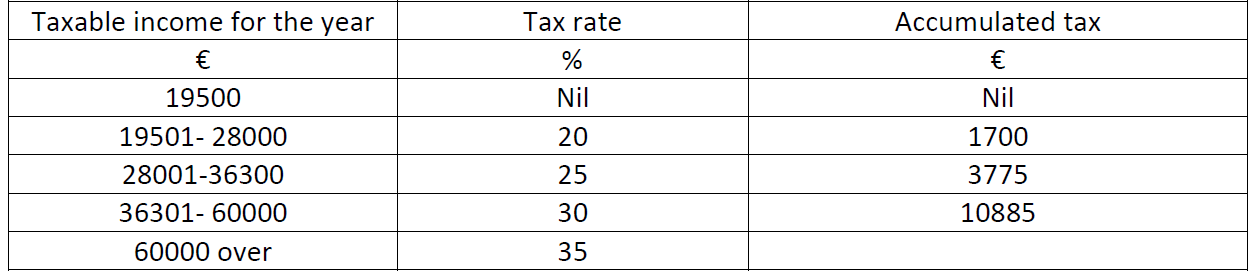

Income tax rates are progressive, and the first €19.500 of income is taxed at zero rate. The first taxable band is taxed at 20% with the highest band starting at over €60.000 taxed at 35%. See Appendix A.

These taxes apply to active income received by Non Doms, such as salary, services, emoluments etc.

Appendix A

Special Defense Contribution tax for Non Doms

This tax is applied to passive types of income.

All types of income listed immediately above are also subject to a contribution of 2.65% towards the General Healthcare System, with a maximum cap of Euro 180,000.

Executive summary:

This is an attractive regime aimed to encourage foreign shareholders of companies and/or individuals with passive income to reside in Cyprus.

In addition, in case the recipient has active types of income, the income tax rules offer generous exemptions for first time residents for a number of years, allowing for a significantly lower effective income tax rate.